|

A catastrophe, as defined by the insurance industry, is a natural disaster that causes a certain dollar amount, currently set at $25 million in insured damage. Individual insurance companies may declare a "catastrophe" based on the anticipated loss to their policyholders in the impacted area. In most cases, that means they will set up special claims processing centers, establish 24-hour emergency hotlines and send in additional, specially trained claims adjusters to the scene of the catastrophe. These "catastrophe teams" generally arrive as soon as possible and stay as long as they are needed.

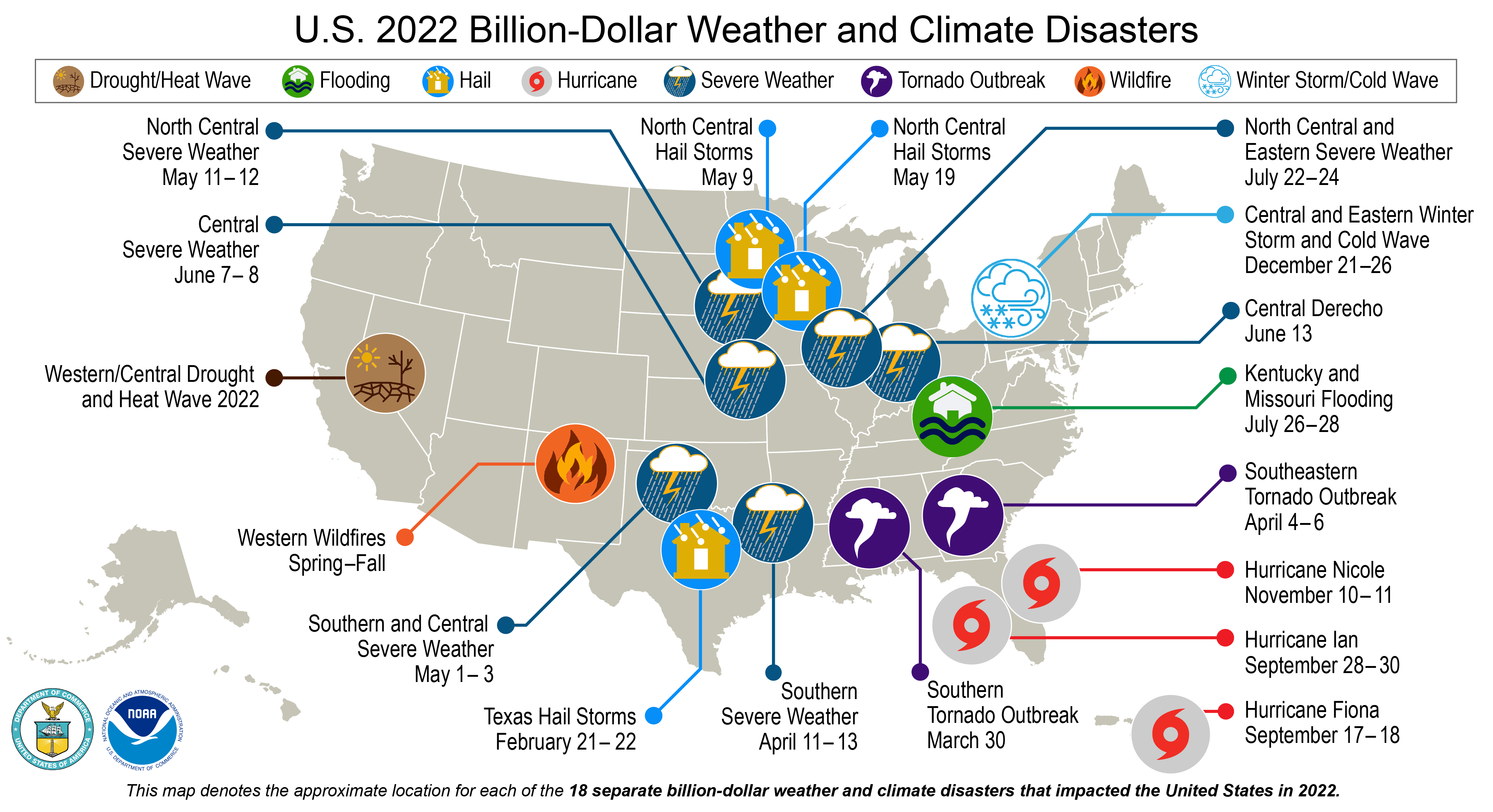

Natural catastrophe losses in the United States rose to an historic high in 2017 of $130.9 billion, the year of Hurricanes Harvey, Maria and Irma and costly California wildfires. Natural catastrophe losses fell 55 percent in 2018 and 36 percent in 2019, when they totaled $38.7 billion. In 2020 they rose 111 percent to $81 billion and rose again to $91 billion in 2021. Source: Insurance Information Institute

Flooding is the most common natural disaster; however, coverage for flood (defined as rising water) is excluded under most standard homeowners policies. For cars, flooding is covered under the comprehensive portion of most standard auto policies. Homeowners and renters who live in high-risk flood plains and whose communities participate in the National Flood Insurance Program, or NFIP (administered by the federal government), can buy special flood insurance through a company or agent.

In March 2023 APCIA (American Property Casualty Insurance Association) released a white paper outlining the Property Market Catastrophe Trends. This white paper looks at inflation, natural disasters, and more straining property insurance markets. Click here to read more.

Rocky Mountain Region Statistics

Over the last 20 years, Colorado has seen the occurrences of natural disasters increase by 275%. The only state with a larger increase during that time is Kansas, which saw a jump of 288%. Consider this. Between 1982 and 2001 there were 12 natural disasters in Colorado. But, from 2002 to 2021, the state has experienced a total of 45 damage-causing natural events. Drought, wildfires, and floods have been major culprits in Colorado.

Over the last 40 years in Colorado alone, the cost of natural disasters is between $20 billion and $50 billion. In states like California and Florida, the cost is in the neighborhood of $200 billion.

Volatile catastrophe trends stemming from destructive hailstorms and wildfires are having a significant impact Colorado's homeowners insurance market—both in terms of the number of damage claims and average claims costs. According the Insurance Research Council's Trends in Homeowners Insurance, 2015 Edition, from 2009-2013, Colorado experienced a 179% increase in the average claim payment per insured home compared to the previous 12 years—the largest percentage increase in the U.S. In fact, 54% of Colorado homeowners insurance claims were catastrophe-related. Click here for IRC findings on Colorado homeowners insurance trends.

- Colorado ranks 2nd in the U.S. for hail insurance claims. May 8, 2017 recorded the state's most costly hailstorm with $2.3 billion in insured losses. Source: RMIA and NICB

- Colorado's 2018 hail season resulted in three carastrophic storms totaling an estimated $618 million in insured losses and more than 100,000 auto and homeowners claims (RMIA) NOAA economic loss estimates rank the storms that hit Colorado's Front Range/SE Wyoming/Southern CO (June) and Southern CO/Plains (August) as billion-dollar disasters.

- The 1990 hail storm resulted in $625 million in actual dollars paid out, but when adjusted for inflation, it totaled $1.37 billion in 2022 dollars.

- The most costly wildfire in Colorado history is the December 30, 2021 Marshall Fire in Boulder County and while recovery is still in progress insured preliminary insured damage estimates top at least $2 billion with 1,089 lost and 149 significantly damaged

- The most destructive wildfire in Colorado history is the June 2013 Black Forest Fire. Estimated insured losses totaled $420.5 million ($518 million in 2022 dollars) resulting from approximately 4,173 homeowner and auto insurance claims filed. El Paso County reports 486 structures burned in the blaze.

- Windsor, Colorado experienced a tornado and hail storm in May 2008 causing an estimated $257 million in insured losses when adjusted for inflation (2022).

- The September 2010 Fourmile Canyon Fire burned 169 homes and other personal property in the foothills just northwest of Boulder. Damage estimates totaled $217 million ($286 million in 2022 dollars) from insurance claims that included smoke damage, additional living expenses, damaged and destroyed homes, as well as personal belongings and vehicles.

- The June 2012 High Park Fire near Fort Collins burned 259 homes, and based on the 1,293 insurance claims filed, the insurance costs are estimated at $113.7 million ($142 million in 2022 dollars).

- The overall estimated cost of the 2002 Iron Mountain, Coal Seam, Missionary Ridge and Hayman Fires in Colorado is $70.3 million in insured losses ($112 million in 2022 dollars). Companies took in about 1,236 claims for the Hayman and Missionary Ridge Fires at an estimated cost of $56.4 million ($90 million in 2022 dollars).

- In 2000, wildfire caused an estimated $140 million in insured losses to some 220 homes in Los Alamos, New Mexico ($233 million in 2022 dollars).

- The blizzard of March 2003 was the most expensive winter storm from snow and ice damage in Colorado history. The estimated price tag was nearly $93.3 million ($145 million in 2022 dollars) from more than 28,000 claims filed.

- In June of 1990, a tornado touched down in Limon, Colorado causing an estimated $20 million ($43 million in 2022 dollars) in insured damages.

- A hailstorm in Albuquerque, New Mexico on October 5, 2004, caused about $39.7 million ($60 million in 2022 dollars) in insured losses.

- May 10, 2005, Hobbs, New Mexico's hailstorm caused approximately $21 million ($30 million in 2022 dollars) in insured losses.

- In June 2005, Lovington, New Mexico experienced $13.7 million ($20 million in 2022 dollars) in claims resulting from hail.

- Colorado's most costly catastrophes have primarily been hail storms over the Denver-metro area (largest concentration of population and, therefore, property damage).

Most Costly Catastrophes in the Rocky Mountain Region (in order of cost)

| Year |

Peril |

Insured Loss

($ Millions) |

2022 Dollars

($ Millions)* |

| May 8, 2017 |

Hail - Denver Metro |

$2.3 Billion |

$2.6 Billion |

| December 30, 2021 |

Wildfire, Marshall, Boulder County |

$2 Billion |

$2.1 Billion |

| July 20, 2009 |

Hail and wind - Denver Metro |

$767.6 |

$1 Billion |

| July 1990 |

Hail - Colorado |

$625.0 |

$1.37 Billion |

| October 2020 |

Wildfire - East Troublesome, Grand County |

$543 |

$602 |

| June 2012 |

Wildfire - Colorado Springs, Colorado |

$453.7 |

$568 |

| June 2013 |

Wildfire - Black Forest, Colorado |

$420.5 |

$518 |

| June 6-15, 2009 |

Tornado and hail - Denver Metro |

$353.3 |

$473 |

| June 6-7, 2012 |

Hail - Colorado |

$321.1 |

$402 |

| June

1984 |

Hail - Colorado |

$276.7 |

$765 |

| July 29, 2009 |

Hail - Pueblo, Colorado |

$232.8 |

$311 |

| October

1994 |

Hail - Colorado |

$225.0 |

$436 |

| September 2010 |

Wildfire - Boulder, Colorado |

$217.0 |

$286 |

| September 29, 2014 |

Hail - Colorado |

$213.3 |

$259 |

| May 2008 |

Tornado and hail - Windsor, Colorado |

$193.5 |

$258 |

| July 13, 2011 |

Hail - Colorado Front Range |

$164.8 |

$210 |

| June

2004 |

Hail - Colorado |

$146.5 |

$222 |

| May-June

2000 |

Los Alamos Fire - New Mexico |

$140.0 |

$233 |

| August

1997 |

Hail - Colorado |

$128.0 |

$229 |

| May 1996 |

Hail - Colorado |

$122.0 |

$223 |

| July 11, 2011 |

Hail - Cheyenne, Wyoming |

$120.0 |

$153 |

| June 2012 |

Wildfire - near Ft. Collins, Colorado |

$113.7 |

$142 |

| June 1991 |

Hail - Colorado |

$100.0 |

$211 |

| March 2003 |

Winter storm - Colorado |

$93.3 |

$145 |

| October 1998 |

Hail - Colorado |

$87.8 |

$154 |

| October 2020 |

Wildfire - Cameron Peak |

$71 |

$78 |

| Summer 2002 |

Wildfires - Colorado |

$70.3 |

$112 |

| August 2004 |

Hail - Colorado |

$62.2 |

$94 |

| October 2004 |

Hail - Albuquerque, New Mexico |

$39.7 |

$60 |

| May 2005 |

Hail - Hobbs, New Mexico |

$21.0 |

$30 |

| June 1990 |

Tornado - Limon, Colorado |

$20.0 |

$43 |

*2022 estimated costs calculated according to the Insurance Information Institute with adjustment from 2022 consumer price index.

Top Catastrophes in the Rocky Mountain Region (in order of occurrence)

| Year |

Peril |

Insured Loss

($ Millions) |

2022 Dollars

($ Millions)* |

| June 1984 |

Hail - Colorado |

$276.7 |

$765 |

| June 1990 |

Tornado - Limon, Colorado |

$20.0 |

$43 |

| July 1990 |

Hail - Colorado |

$625.0 |

$1.37 Billion |

| June 1991 |

Hail - Colorado |

$100.0 |

$211 |

| October 1994 |

Hail - Colorado |

$225.0 |

$436 |

| May 1996 |

Hail - Colorado |

$122.0 |

$223 |

| August 1997 |

Hail - Colorado |

$128.0 |

$229 |

| October 1998 |

Hail - Colorado |

$87.8 |

$154 |

| May-June 2000 |

Los Alamos Fire - New Mexico |

$140.0 |

$233 |

| Summer 2002 |

Wildfires - Colorado |

$70.3 |

$112 |

| March 2003 |

Winter storm - Colorado |

$93.3 |

$145 |

| June 2004 |

Hail - Colorado |

$146.5 |

$222 |

| August 2004 |

Hail - Colorado |

$62.2 |

$94 |

| October 2004 |

Hail - Albuquerque, New Mexico |

$39.7 |

$60 |

| May 2005 |

Hail - Hobbs, New Mexico |

$21.0 |

$30 |

| May 2008 |

Tornado and hail - Windsor, Colorado |

$193.5 |

$258 |

| June 6-15, 2009 |

Tornado and hail - Denver Metro |

$353.3 |

$473 |

| July 20, 2009 |

Hail and wind - Denver Metro |

$767.6 |

$1 Billion |

| July 29, 2009 |

Hail - Pueblo, Colorado |

$232.8 |

$311 |

| September 2010 |

Wildfire - Boulder, Colorado |

$217.0 |

$286 |

| July 11, 2011 |

Hail - Cheyenne, Wyoming |

$120.0 |

$153 |

| July 13, 2011 |

Hail - Colorado Front Range |

$164.8 |

$210 |

| June 6-7, 2012 |

Hail - Colorado Front Range |

$321.1 |

$402 |

| June 2012 |

Wildfire - near Ft. Collins, Colorado |

$113.7 |

$142 |

| June 2012 |

Wildfire - Colorado Springs, Colorado |

$453.7 |

$568 |

| June 2013 |

Wildfire - Black Forest, Colorado |

$420.5 |

$518 |

| September 29, 2014 |

Hail - Colorado |

$213.3 |

$259 |

| July 28, 2016 |

Hail - Colorado Springs |

$352.8 |

$422 |

| May 8, 2017 |

Hail - Metro Denver |

$2.3 Billion |

$2.6 Billion |

| October 2020 |

Wildfire - East Troublesome |

$543 |

$603 |

| October 2020 |

Wildfire - Cameron Peak |

$71 |

$78 |

| December 2021 |

Widfire - Marshall |

$2 Billion |

$2.1 Billion |

*2022 estimated costs calculated by the Insurance Information Institute with adjustment from 2022 consumer price index.

National Statistics

-

Hail-related insured losses between 2000 and 2019 averaged between $8 billion to $14 billion a year, according to Aon. There were 3,763 major hailstorms in 2021, according to the NOAA’s Severe Storms database.

-

Hurricane Katrina was the costliest natural catastrophe, causing $65 billion in damage when it occurred in 2005, including losses from the NFIP. Katrina would cost $95 billion in 2022 dollars. Seven additional hurricanes made the top 10 list, including Hurricane Sandy in 2012, which caused $30 billion when it occurred and Hurricanes Harvey, Irma and Maria in 2017, each of which also caused about $30 billion in losses. Hurricanes Andrew, Ike and Wilma are also included in the top 10.

-

The 1994 Northridge quake was the costliest U.S. earthquake on record, causing $15.3 billion in insured damages when it occurred ($29.6 billion in 2022 dollars). Six of the costliest U.S. quakes, based on inflation-adjusted insured losses, were in California.

- In 2021, there were there were 1,376 tornadoes in the United States, compared with 1,075 in 2020, according to preliminary data from the National Oceanic and Atmospheric Administration (NOAA).

According to the Insurance Information Institute - 2021 Fact Book

Ten Most Costly Catastrophes in the United States

| Month/Year |

Peril |

Insured Loss

($ Billions) |

2022 Dollars

($ Billions) |

| 1. Aug. 2005 |

Hurricane Katrina |

$41.1* |

$60 |

| 2. Oct. 2012 |

Hurricane Sandy |

$30 |

$37 |

| 3. Aug. 2017 |

Hurricane Harvey |

$30 |

$35 |

| 4. Sept. 2017 |

Hurricane Irma |

$29.9 |

$35 |

| 5. Sept. 2017 |

Hurricane Maria |

29.6 |

$34 |

| 6.Aug. 1992 |

Hurricane Andrew |

$16 |

$32 |

| 7. Jan. 1994 |

Northridge, CA Earthquake |

15.3 |

$29 |

| 8. Sept. 2008 |

Hurricane Ike |

$18.2 |

$24 |

| 9. 2012 |

Drought Loss |

$14.3 |

$17 |

| 10. Oct. 2005 |

Hurrican Wilma |

$10.6 |

$15 |

*The National Flood Insurance Program paid $16.3 billion in Katrina claims, in addition to the $41.1 billion paid by private insurers.

Sources: Insurance Services Office, Inc. (ISO) & Insurance Information Institute with adjustment from 2022 consumer price index

U.S. Catastrophe Record 2001 - 2020

The following chart shows the number of catastrophes causing insured property losses of at least $25 million.

| Year |

Number of Catastrophes |

Claims ($ Millions) |

Insured Losses ($ Billions) |

2022 Dollars ($ Billions) |

| 2001 |

20 |

1.6 |

$26.5 |

$43 |

| 2002 |

25 |

1.8 |

$5.9 |

$12 |

| 2003 |

21 |

2.6 |

$12.9 |

$20 |

| 2004 |

22 |

3.4 |

$27.5 |

$41 |

| 2005 |

24 |

4.4 |

$62.3 |

$91 |

| 2006 |

31 |

2.3 |

$9.2 |

$13 |

| 2007 |

23 |

1.2 |

$6.7 |

$9.2 |

| 2008 |

36 |

4.1 |

$27.0 |

$36 |

| 2009 |

27 |

2.2 |

$10.5 |

$14 |

| 2010 |

33 |

2.4 |

$14.3 |

$18 |

| 2011 |

30 |

4.9 |

$33.6 |

$42 |

| 2012 |

26 |

4.0 |

$35.0 |

$43 |

| 2013 |

28 |

1.8 |

$12.9 |

$15.9 |

| 2014 |

31 |

2.1 |

$15.5 |

$18 |

| 2015 |

39 |

2.0 |

$15.2 |

$18 |

| 2016 |

42 |

3.0 |

$21.7 |

$25 |

| 2017 |

46 |

5.2 |

$101.9 |

$119 |

| 2018 |

55 |

|

$60.4 |

$69 |

| 2019 |

|

|

$38.7 |

$44 |

| 2020 |

|

|

$74.4 |

$82 |

| 2021 |

|

|

$92 |

$97 |

Sources: Insurance Services Office, Inc. (ISO) & Insurance Information Institute with adjustment from 2022 consumer price index

What To Do in a Catastrophe

Residents evacuated from their homes should contact their insurance agents or companies immediately and let them know where they can be reached. As adjusters are allowed into impacted areas, they will want to go in with their policyholders to access the extent of the damage. In the event of a catastrophe situation, many insurance companies set up 24-hour emergency hotlines.

Company claims adjusters, many equipped with laptop computers and portable phones, will start writing checks to pay the cost of temporary living expenses for people left homeless by catastrophes and to begin the rebuilding of damaged homes. Some companies will open special claims centers to assist their policyholders. Contact your agent or company if you need additional living expenses while you are out of your home.

Keep receipts.

Out-of-pocket expenses during a mandatory evacuation are reimbursable under most standard homeowner policies.

Be prepared to give your agent or insurance representative a description of your damage.

Your agent will report the loss immediately to your insurance company or a qualified adjuster who will contact you as soon as possible to inspect the damage. Again, be sure to give your agent a number where you can be reached.

Take photos of the damaged areas.

These will help with your claims process and will assist the adjuster in the investigation.

Prepare a detailed inventory of all damaged or destroyed personal property.

Be sure to make two copies-one for yourself and one for the adjuster. Your list should be as complete as possible, including a description of the items, dates of purchase or approximate age, cost at time of purchase and estimated replacement cost.

Make whatever temporary repairs you can.

Cover broken windows, damaged roofs and walls to prevent further destruction. Save receipts for supplies and materials you purchase. Your company will reimburse you for reasonable expenses in making temporary repairs.

Secure a detailed estimate for permanent repairs to your home from a reputable contractor and give it to the adjuster. The estimate should contain the proposed repairs, repair costs and replacement prices.

Serious losses will be given priority.

If your home has been destroyed or seriously damaged, your agent will do everything possible to ensure that you are given priority.

Disaster Planning

Do you know what to do in the event of a disaster? Are you ready if a fire, flood, or tornado strikes your home? It may not be fun to think about, but it never hurts to plan ahead - especially if you live in a disaster-prone area. Know where you should go, who you should notify, and what to bring. A great resource for disaster-planning is FEMA's "Are You Ready?" and Safety.com Emergency Preparedness, they walk you through steps you and your family can take so that you are better prepared should a disaster strike.

Do you want to know how to prepare your home in the event of a Natural Disaster? MoneyGeek has a great website that will help you do just that! Please visit Emergency Preparedness: How to Get Your Home Ready for a Natural Disaster.

Disasters can and will cause stress to families and individuals. FEMA's Coping with Disaster page offers disaster survivors informaiton regarding dealing with the emotional affects of the event. This page gives guidance related to recognizing the signs of and minimizing the impact of disaster-related stress. Please remember that reactions and risk response to disasters vary, and there are many different signs of disaster-related stress. Support during this time is important for all who experience a disaster, especially children, older adults, and vulnerable individuals.

Last House Standing: http://flash.org/lasthousestanding/

Do you have what it takes to build the most awesome house around? One that wins you bragging rights and can withstand the worst of Mother Nature? Developed by the Federal Alliance for Safe Homes (FLASH), Last House Standing is a social gaming app that provides the ultimate design and disaster challenge. Players have three minutes and $100,000 to build a house that strikes a perfect balance between stylish and indestructible. When it's finished, the game will unleash Mother Nature's wrath. Whatever is left will be judged on flair and survivability. Challenge random opponents and friends to see who will have the Last House Standing. By making preparedness fun and accessible, Last House Standing can breakdown the common "where to begin" disaster safety barrier.

|

|